The Seattle City Council this week got a revenue forecast update from the City Budget Office, useful for developing the 2022 budget. The revenue forecast was generally good news, but there are some dark clouds in the sky, notably in lagging employment, hospitality and manufacturing sectors, and downtown office vacancies and commercial construction.

The federal stimulus package seems to have done the trick, and in the second quarter of 2021 the local economy took off. Despite warnings that people were holding their stimulus checks in their bank accounts, it turns out a lot of people went out and spent them. Personal outlays skyrocketed in the second quarter, and retail sales (and sales taxes) followed suit.

As recently as April economists were giving equal probabilities for “baseline” and “pessimistic” national economic forecasts, given the unclear timeline for the next federal stimulus package and the slow rollout of COVID vaccines. But here’s a graph of how much the economy outperformed “baseline” and “pessimistic” scenarios in the first half of 2021 (mainly the second quarter):

You can see that personal outlays and retail sales dramatically outperformed even the baseline scenario.

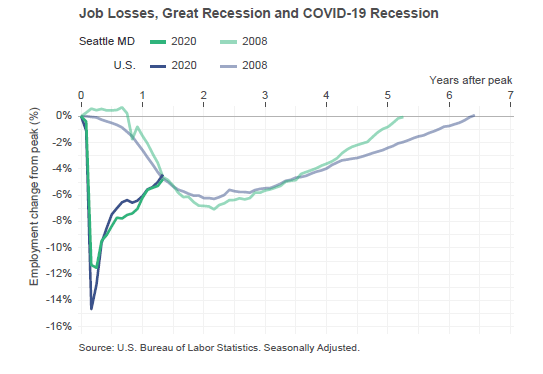

Employment is a different story altogether. Both nationally and in Seattle, employment is recovering more slowly — but in a different way than in past recessions. The drop in jobs happened dramatically, with a very speedy partial recovery, and then it shifted into low gear (with some signs that it might be starting to pick up again). Currently both nationally and locally we’re off about 4.5% from pre-pandemic employment levels.

However, job openings are now at a record high, and wages are significantly up.

At the moment, this unusual situation is being attributed to a shortage of workers, driving up salaries. Economists cite several contributing factors to the worker shortage:

- Coming out of the pandemic, labor force participation is low. Many people simply chose to retire when the pandemic hit, while some have a bit of a cushion because of unemployment benefits and relief checks and are taking their time in choosing their next job.

- Some workers moved during the pandemic. It’s unclear whether they will move back as it subsides.

- Some are still worried about the health risks of returning to work or are still caring for family members and aren’t yet free to enter the workforce.

Here’s a graph of what’s happened to employment in the Seattle metropolitan district (MD) compared to pre-pandemic. Some sectors are approximately back to where they were 18 months ago; but manufacturing has still been hit hard, and the hospitality industry is only now starting to come back to life.

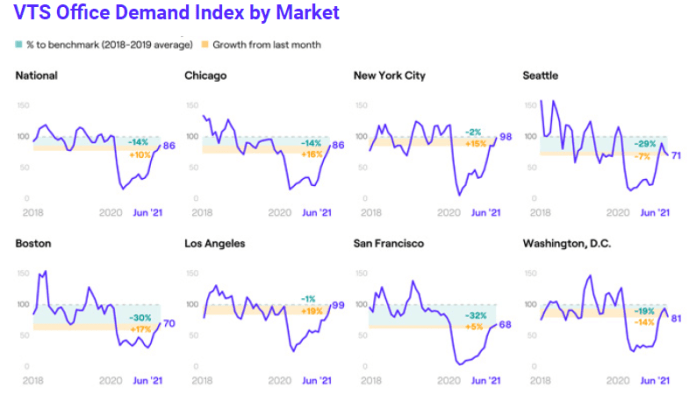

Nationally office space vacancy rates are running a few percentage points higher than before the pandemic, but in Seattle and neighboring cities, it’s much worse. In Seattle’s central business district, vacancy rates are over 20%. In Seattle’s case, it is suffering from having a bounty of “remote-friendly” jobs, which is depressing demand for office space.

Seattle’s office demand as of June 2021, as measured by real estate technology firm VTS, was only at 71% of pre-pandemic levels. Worse, it actually dropped seven points in the second quarter.

We can see this reflected in the count of office workers downtown, which is still at 20% of 2019 levels and is not budging.

The downstream effect of the lack of demand for office space will hit the construction sector. Commercial real estate is well off its pre-pandemic level, though residential construction is partially offsetting it. This continues trends that pre-date the pandemic: new permits for commercial construction have been in the tank since 2018, while the backlog of issued permits was being built. Now commercial construction has dropped even further.

(One note of explanation on the above graph: the large, brief spikes in “permit intake,” aka new permit applications, are tied to the dates where new, more restrictive zoning and construction regulations take effect, as developers rush to vest their project with the old rules just before the deadline.)

So in short, the economic analysis tells us:

- consumer spending and retail sales are strong;

- employment is recovering slowly, despite lots of job openings and increased wages;

- the demand for office space is low, which combined with Seattle’s remote-friendly job base and new COVID delta variant scares means that downtown is not yet bouncing back and the commercial construction sector is in the doldrums.

How does all this affect the city’s economic and revenue forecasts? Given that in the second quarter the national economic indicators tracked with the baseline model and economists have now shifted to a 50% probability of the baseline forecast being correct (and only 20% probability for the pessimistic model), the City Budget Office has now switched to basing its revenue estimates on the baseline instead of the pessimistic forecast. Those forecasts predict that national employment should return to pre-pandemic levels by the end of 2022, and by then personal outlays should be tracking with the expected trendline before COVID hit.

The forecasts for the Seattle metropolitan district are very similar, with even more dramatic upward revisions.

That’s the good news. The bad news is that inflation has also been revised up, with the national CPI-U now projected at 3.7% for 2021, and the Seattle area CPI-W for July 2021 through June 2022 forecast at 4.8% (up from 2.8% previously).

The City Budget Office gave the Council one more jolt of good news this week. With the booming economy in the second quarter, several categories of revenues are running significantly over forecast — and total revenues are now expected to come in over $52 million higher for the year. Nearly all of the additional revenue is “general fund,” which gives the city the most flexibility in how to spend it. Over $36 million of that is two line-items: sales taxes and B&O taxes, which is consistent with the increase in consumer spending we’ve seen in the data. The city also recalculated its payroll tax projections using updated employment figures from the state, and revised upward its 2021 revenue estimate by $3.4 million to a new total of $217.7 million.

In addition, with the early reopening of the economy admissions taxes are now projected higher. However, REET revenue (based on real estate transactions) estimates are unchanged: real estate prices are higher, but the volume of transactions is lower.

The numbers aren’t quite as rosy for 2022, though they are still quite good. B&O tax continues to roar back according to the city’s projections, but earlier forecasts had already built in assumptions of a fairly robust recovery in 2022 so there isn’t much additional upside.

At the same time, there are some one-time windfalls that need to be taken into consideration. This year the city recognized $66.5 million in income from the sale of the Mercer Megablock property. It also got a huge amount of federal COVID relief dollars, both the first tranche of its ARPA funding and some specific federal program grants. Next year Seattle will get its second and last tranche of ARPA funding, but it’s unclear what it might get from a federal infrastructure bill — assuming Congress passes one. But the city will also have payroll tax revenues to offset the loss of grant funding. By the city’s estimate, general government resources will be about $1.74 billion in 2022, $35 million less than this year’s current forecast.

That brings us back to this year’s revised revenue forecast, which is now a $52 million wad of cash burning a hole in the City Council’s pocket. There will, of course, be temptations to spend some or all of it this year. Perhaps the biggest limit on that will be time, since there is little time for the Council to consider additional spending bills this year. The Council might simply decide to carry over the excess revenues into 2022 and use them to offset the slight decrease in expected revenues next year.

Discover more from Post Alley

Subscribe to get the latest posts sent to your email.

{kind=link}

The data are alarming, and Seattle may have to face structural problems, not just covid: it’s overbuilt, too dependent on Amazon (which has stopped growing in Seattle), too expensive, too congested, and too dysfunctional politically. Why is there not a respected Jeremiah around? Instead, we get almost all glass-half-full commentary. Bah!

IMO the biggest problem facing Seattle, King County, and Washington State is the willingness of officials to disregard the obvious: remote working policies by the employers that used to demand hundreds of thousands of daily commutes to and from downtown Seattle mean all the land use and transportation plans need significant changes.

The new normal is staring everyone in their faces. Tech especially will continue to embrace distributed workforces. Over half the residents of Seattle earn their (big) paychecks from home. As the new normal is productive (due to broadband, effective communication apps, etc.) all over the country and more so here it is revolutionizing what a job is for most residents of this part of the world.

The government officials calling the shots are not even studying the trends, data or implications. Everywhere else the new normal for tech and other jobs that use computers is studied widely:

https://www.minneapolisfed.org/research/institute-working-papers/the-geography-of-remote-work

https://www.mass.gov/doc/future-of-work-in-massachusetts-report/download

What’s the problem with government here that keeps it fixated myopically on planning for growing levels of daily commuters to offices in the business district that will not materialize? It’d be great to get the viewpoints of the journalistic and political éminences grises comprising Post Alley. It strikes me as fear: they’ve built their careers sucking up to skyscraper developers, union lobbyists, and other government officials who’ve benefitted from upzoning and taxing regressively for transit, so to even acknowledge that the best path forward for people involves less of those two things produces cognitive dissonance.